How to transfer money to Europe

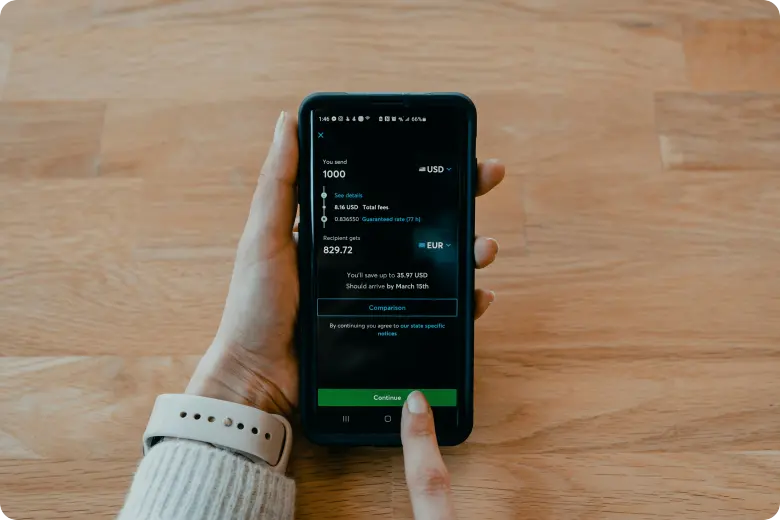

To transfer money to Europe, you need three things: a sending account, a receiving method, and a provider that supports the currency route you need.

For immigrants in Portugal or Spain, the final destination is usually a euro account. That could be your Portuguese bank account, your Spanish bank account, a fintech account with a European IBAN, or another person’s account in Europe.

Start with the purpose of the transfer

The best way to send money depends on why you are sending it.

For salary, pension or freelance income

If you receive income from abroad, a fintech account can help you receive money in one currency and convert it to euros before sending it to your local bank account.

For example, someone earning in USD while living in Portugal may use a provider that gives local USD account details. The money can arrive as a local US payment, then be converted to euros and moved to a Portuguese account.

For rent, bills, and daily life

A local Portuguese or Spanish bank account is often useful for rent, utilities, direct debits, tax refunds, and administrative proof. Even if you use fintech apps, a local account can make life easier when dealing with landlords, public services, or traditional institutions.

For family support

If you need to send money to family members who do not use bank accounts, remittance providers with cash pickup or mobile wallet options may be more practical than a bank transfer.

For large transfers (more than 20K)

If you are moving savings, buying property, or transferring business funds, use a traceable provider and keep documents showing where the money came from. Larger transfers can trigger extra checks from banks or payment providers.